Italian Exhibition Group S.p.A.

Microcap with atractive growth and a cheap valuation.

Introduction

Italian Exhibition Group SpA (MIL:IEG, ISIN IT0003411417) is a business organizing trade fairs and exhibitions in Italy and abroad. It IPO’d in 2019 at an offering price of euro 3.70 a share. It is currently trading at 2.75 euro a share after suffering during the pandemic. Only recently has IEG shown signs of recovering. At mid-single digit earnings multiples I believe it represents an attractive investment opportunity.

Business overview

IEG operates across 5 business lines:

Organized Events - the organization and implementation of events across five categories: (i) food and beverage; (ii) jewellery and fashion; (iii) tourism, hospitality and lifestyle; (iv) wellness and leisure; and (v) green and technology. This is the highest margin segment.

Hosted Events - renting out exhibition facilities to third party organizers.

Conferences - promotion and management of conference events.

Related Services - providing services related to exhibitions and congresses. Things like catering and exhibition stand installation.

Publishing, Sporting Events and Other Activities - rentals of advertising space and other non-core activities. Only 1% of total revenue.

The image below shows the composition of IEG’s revenues.

The events organized in Italy are mostly in the following structures:

Quartiere Fieristico (Trade Fair District) of Rimini, located in via Emilia no. 155

Quartiere Fieristico (Trade Fair District) of Vicenza, situated in via dell’Oreficeria no. 16

Palacongressi di Rimini, located in via della Fiera no. 23 in Rimini

Vicenza Convention Centre, in via dell’Oreficeria no. 16

The two trade fair districts are owned by IEG. The Rimini Expo center is leased and the Vicenza center is part owned and part leased, with the lease expiring on 31 December 2050.

IEG also organizes events in Brazil, Mexico, the US, China and Dubai.

Finances

Revenues have started to recover post pandemic. H1 2023 revenues have more than doubled yoy, however part of that is because they are lapping easy comps as H1 2022 was still somewhat effected by covid measures. Margins have started to expand as well and in Q4 2022 and Q1 2023 the net margin was slightly above 15%. Ytd revenue stands at 119 million euro and net income at 10.6 million euro.

IEG currently has net debt of roughly 95 million euro’s. They have 42 million in liquidity. The debt seems scarier than it really is in my opinion. The majority of the debt, about 100 million euros, are mortgages owed to different banks. The mortgages are made up of the following loans (as of 31 March 2023 in thousands of euros):

Non-current:

Banca Intesa mortgage - 27,593

Credit Agricole pool mortgage - 8,367

SACE mortgages - 5,977

Other group company loans and mortgages - 2,497

Total non-current - 89,645

Current:

Banca Intesa mortgage - 1,733

Credit Agricole pool mortgage - 1,838

SACE mortgages - 5,977

Volksbank mortgage - 684

Other group company loans and mortgages - 2,559

Total current - 12,791

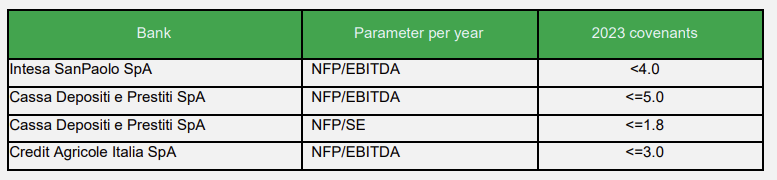

The covenants on the debt:

It is important to note that IEG briefly breached the covenants on one of their mortgages. From their Q1 report:

At 31 December 2022, the covenant breach occurred in connection with the NFP/EBITDA ratio (covenant < 3.5) related to the loan stipulated by the Parent Company with Credit Agricole Italia Spa (the pool Agent Bank). On 5 December, the Parent Company asked that the application of the covenant be suspended for FY 2022; this request was granted on 10 March 2023. Following this reply, the non-current portion of the pool loan was reclassified for 8,367 thousand euros.

At time of writing IEG has a NFP (Net Financial Position) of 94.838 million, TTM EBITDA of 41.3 million and shareholders’ equity of 105.169 million. In my opinion the company should have no problem being in compliance with these covenants again.

Plans for the future

In this investor presentation from July 2022, IEG explains their strategic plans and goals for the 2022-2027 period. I highly recommend reading through this presentation if you’re interested in IEG. In short, their plans consist of growth through expansion and acquisitions. In the coming years they will expand the expo center in Vicenza and possibly the center in Rimini as well. The acquisitions consist of small deals internationally. They have a history of doing small bolt-on acquisitions and in their filings they do a good job of explaining recent ones. Up until this point these acquisitions have been financed by cash flows from the company. They plan to finance future expansion with cash flows as well, however they are also exploring the possibility of a convertible bond offering of 40 million euros. These possible bonds would be issued in 2024 and mature in 2028. A decision is expected in the summer of 2023. As far as I am aware nothing has been decided yet, so I would expect some clarity fairly soon.

The financial targets for 2027 are revenue of 267 million with EBITDA of 69 million. They plan to bring their net financial position down to 41 million, so they are deleveraging the balance sheet. Additionally they indicate they’ll start paying a dividend in 2024.

Controlling shareholder

Rimini Congressi S.r.l. owns a 50.01% stake in IEG. As far as I can tell, Rimini Congressi is a holding company controlled by local government entities. The three main shareholders in Rimini Congressi are the Rimini Municipality, Province of Romagna and the local chamber of commerce. However, since I don’t speak Italian and Rimini Congressi doesn’t have a website in English, I have to rely on translations, so I might be wrong on the majority shareholder.

Valuation

Taking managements 2027 targets of 69 million in EBITDA and net debt of 41 million at face value and assuming a 10 EV/EBITDA multiple we get to a stock price of ~21 euros. Given the recent strong performance I think revenue estimates of 267 million in 2027 are very reasonable. Assuming a 7% net margin (which is in line with what they have done pre-pandemic) you get net income of ~19 million. This implies a PE of ~5. I actually think this is very conservative as they should benefit from a larger scale and so margins should expand. In fact, in recent seasonally strong quarters they had net margins around 15%. However, it never hurts to be conservative. All in all, I think we can expect earnings growth and margin expansion resulting in a stock price in 2027 that is a few times what it is today.

My twitter: @rauwkost1

Disclosure: I am long IEG