Halyk Savings Bank of Kazakhstan

The largest bank in Kazakhstan is currently trading around 3 times earnings and might soon have a dividend yield of 15+%.

Business summary

The Halyk Savings Bank of Kazakhstan (LSE:HSBK) is the largest bank in Kazakhstan while also operating in Georgia, Kyrgyzstan and Uzbekistan. The bank operates across a variety of segments like retail, SME & corporate banking, insurance, leasing, brokerage and asset management. Although they operate in multiple countries their main market is Kazakhstan. In Kazakhstan they are the largest bank with a retail deposit market share of 32.1% and 575 branches and other outlets across the country. On the 30th of september they owned 236,123 POS-terminals. According to the National Bank of Kazakhstan there were 748,982 POS-terminals in the country on 1-10-2022. This gives Halyk market share of 31.5%. In the retail loan market they got 20% market share with a KZT (Kazakhstani tenge) 2,567bn loan book. In the SME & corporate banking segment Halyk’s market share is equally impressive with loan market share at 52.5% and deposits at 36.5%.

Halyk also provides government services online, some of which are exclusive to Halyk. The services that are exclusive to Halyk are deregistration at the place of residence, submission of a tax declaration, a compulsory pension contributions statement, real estate statement, compulsory social contribution statement and checking information about labor contracts. They offer many more services, a complete list can be found on page 14 of their q3 2022 investor presentation. Furthermore they are the largest payment agent for pensions and social payments. The bank is also one of the leading participants in the fixed income securities market and the foreign currency market. The Bank is a primary dealer in both Treasury Bills of the Ministry of Finance of Kazakhstan and short-term notes of the NBRK (National Bank of Kazakhstan).

Additionally they are currently working on a ‘‘superapp’’ which offers e-commerce, tickets for cinemas and travel. Although this is still in the early stages and they are facing fierce competition from Kaspi (for full disclosure: I am also long Kaspi, LSE:KSPI), the growth has been impressive. The marketplace segment of the app for example has seen merchants go from 335 on 1-10-2021 to 12,595 on 1-10-2022. Although I believe Kaspi will become the leading “superapp“ in Kazakhstan, Halyk can still create a profitable product and combined with their traditional banking services should do well going forward.

The bank is controlled by Timur Kulibayev and Dinara Kulibayev via JSC HG Almex who own 69.7% of shares outstanding. Timur and Dinara are daughter and son-in-law of former Kazakh president Nursultan Nazarbayev.

Rating agencies moody’s, standard and poors and fitch all assign a stable outlook to the bank.

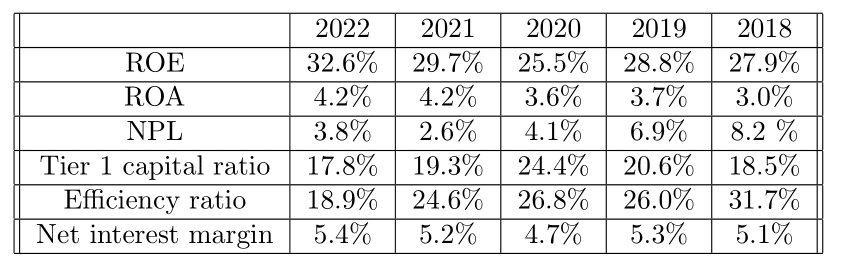

Some numbers

As we can see their ROE and ROA has been fairly stable and even increasing. The cost-to-income ratio has come down significantly which shows the bank is now operating more efficiently than they used to.

Net income has steadily increased in the past few years. This is obviously not a guarantee that the income will continue to increase in the future. Both 2015 and 2016 saw decreases in the net income. In 2015 income fell from 638 million usd to 543 million usd and in 2016 it fell further to 384 million usd. In both years the decrease in net income was due to macro conditions and not the bank’s business model. The price of oil declined and new economic policy was introduced by president Nazarbayev causing uncertainty in markets. Although the decrease in earnings does show Halyk’s dependence on macro conditions it also showed the resilience of the bank as they were still profitable.

The loans to deposits ratio has increased which shows the bank is earning more per tenge deposited. In the past the ratio has fluctuated between 50 and 70%. It shows the bank could be earning more on the deposits but also that it has enough liquidity to cover any requirements.

The values in both tables were taken from the annual reports from 2018-2021. For 2022 the numbers were taken from the q3 report and the net income is for the 9 months ended on september 30.

Macro-environment in Kazakhstan

The economy of Kazakhstan is export-oriented and mainly dependent on commodities such as oil and natural gas. The country is also the world’s largest producer of uranium. Since gaining independence in 1991 the government has implemented reforms to stimulate economic growth and improve the business climate. As a result Kazakhstan now ranks 25th in the World Bank’s Ease Of Doing Business rankings. In topics such as protecting minority investors and enforcing contracts they rank 7th and 4th respectively.

GDP growth is expected to accelerate to 3.5-4.0% in 2023-2024. GDP per capita has steadily increased to 11264.91 usd in 2021. Unemployment currently stands at 4.9% and has been around that level for a decade or so. Like most countries in the world Kazakhstan is currently dealing with high inflation of 19.6%. To combat this the central bank has raised interest rates to 16.75%.

The war in Ukraine so far has had no major impact on the overall economy (or the bank), however this could change if the Caspian Pipeline Consortium (which carries about 80% of Kazakhstan’s oil exports) is shutdown. Kazakhstan is not helping Russia evade sanctions and is seeking to strengthen the economic position of the country.

In january of 2022 there were mass protests in the country. Protesters were discontent with the government and former president Nursultan Nazarbayev. As mentioned his daughter and son-in-law own a controlling stake in Halyk Bank. Although the owners clearly are not well liked in the country, the bank has not suffered from their bad reputation given their strong earnings.

Returns and risks

The bank has a dividend policy to pay out 50 to 100% of total net profits as dividends. Dividends are usually paid out in june, however in 2022 managment decided to postpone the payment to november due to the conflict in Ukraine. Additionally the amount was lowered as well. Should the dividend policy be reinstated, the stock could soon yield 15-20% given that the bank is on track to earn over a billion usd in 2022 with a marketcap of 3 billion.

From 2018 to 2021 the bank has grown net income in usd at 10.15% annually. Given the stable performance of the bank and the expected growth of the Kazakh economy they should be able to continue this growth.

At the current price of 11.20 usd the stock is trading around 3 times earnings. Historically it has traded between 4 and 5 times earnings so a slight multiple rerate might give additional upside.

A deterioration of the macro environment could pose a risk to the bank. Additionally further sanctions against Russia might in the future negatively effect the bank. The bank is monitoring the situation and has no major exposure to sanctioned entities.

Further reading

Allan Gray frontier markets fund having a position in Halyk

Harding Loevner frontier markets fund having a position in Halyk

Disclosure: I hold a material investment in the issuer's securities. This article does NOT constitute advise to buy/sell any of the securities mentioned in the article.

What do you make of regulator blocking the dividend?

https://www.reuters.com/article/kazakhstan-banks-dividend-idUKL1N36T0DQ

This could be politically motivated, given who the majority shareholders are.

How much profit would HSBK need to make to start paying dividends if the regulator is succesful in their attempt?